- Macro Monday

- Posts

- Adding More & More Stimulus Into The Pipeline

Adding More & More Stimulus Into The Pipeline

The Macro Institute's Weekly Economic Primer

The Macro Institute

October 27, 2025

In partnership with

This is starting to feel like Groundhog’s Day, but once again, we’re heading into a light week for data. Even if the government shutdown were to end tomorrow, it would still take time for the BLS and other agencies to catch up on delayed releases.

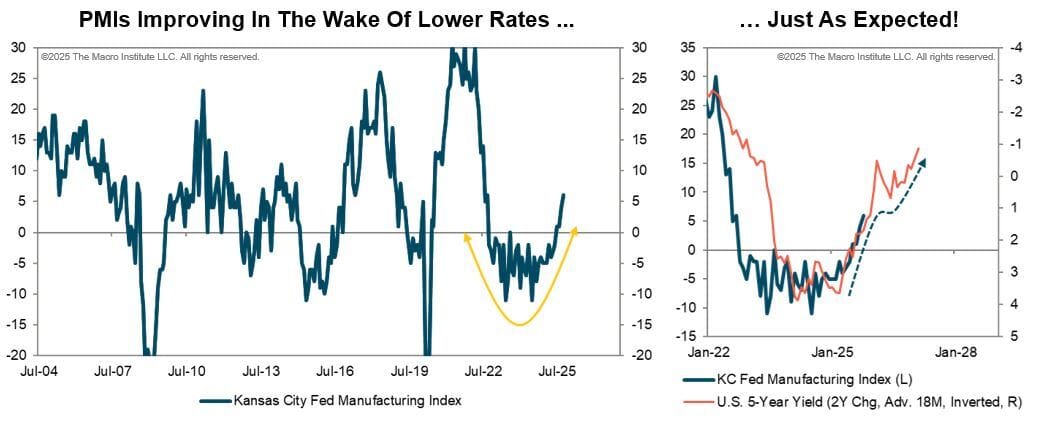

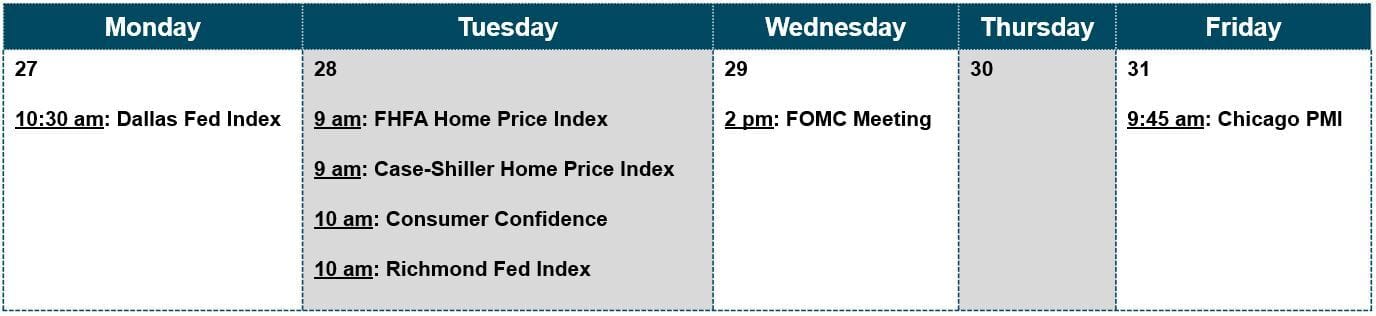

This week, our focus turns to the three regional PMIs being released. The Dallas Fed Index arrives Monday, followed by Richmond on Tuesday, and Chicago on Friday. Interestingly, last week’s Kansas City Fed reading was quite strong. If you remember the old Wall Street adage, “buy the smiles,” that’s exactly what it looked like. We don’t usually spend much time on this series, but it seems to be responding to the lagged effects of lower interest rates, as the clip above suggests. That would argue for more upside in the months ahead. For now, we’ll see if Dallas, Richmond, and Chicago echo that same constructive tone.

The Macro Week In Review

It's not you, it’s your tax tools

Tax teams are stretched thin and spreadsheets aren’t cutting it. This guide helps you figure out what to look for in tax software that saves time, cuts risk, and keeps you ahead of reporting demands.

The Macro Week Ahead

🏎️ Speeding Through The Fog

Equity market momentum continues to build despite the absence of government data and limited updates from private sources. Over the past month, major indices have gained between 2.7% and 3.0%. Beneath the surface, a decline in the U.S. 10-Year Treasury yield helps explain the relative strength in traditionally defensive, Risk-Off, and Risk-Aversion sectors such as Health Care, Technology, Utilities, and Real Estate. This pattern reflects investor expectations for slower growth and lower rates in the months ahead.

At the same time, renewed risk-taking is visible in the outperformance of Small Caps, Emerging Markets, and High Beta stocks. The coexistence of Risk-Off and Risk-On leadership underscores a divided investor base still debating the durability of the current expansion. While a one-month snapshot offers limited conviction, these shifting crosscurrents provide useful insight into evolving market sentiment.

From a cyclical perspective, we remain cautiously optimistic given the significant monetary stimulus still in the pipeline. Historically, such environments tend to support leading indicators of growth and, in turn, equity performance. Our primary concern remains inflation, both near-term and medium-term. We’re watching pressures stemming from tariffs and wage growth that remains above long-run averages. These factors will likely determine how sustainable the recent rally proves to be, as inflation and policy direction typically move together.

📆 The Week Ahead

The S&P 500’s push to new all-time highs on Friday reflected enthusiasm following a softer-than-expected inflation report earlier that morning. Both headline and core CPI for September registered at 3.0%, reinforcing expectations for a rate cut at the upcoming Federal Reserve meeting on Wednesday. While the year-over-year figures eased, giving the bulls some fuel, month-over-month inflation remained firm, tempering some of the optimism.

Betting markets now assign roughly 98% odds to a rate cut this week, up from about 50% a month ago. This shift is driven less by inflation data and more by signs of labor-market cooling. However, the ongoing government shutdown has halted key releases, including the September payrolls report. Markets had braced for another weak employment reading, as a stronger print might have reduced the likelihood of additional easing and pressured equities.

Chairman Powell’s recent remarks suggest he views current policy settings as broadly balanced, placing the Fed in a delicate position with meaningful risks regardless of the decision. Cutting too aggressively could reignite inflation, while tightening might exacerbate the slowdown in employment. In this environment, investors are likely to remain hypersensitive to each new data point and headline, with volatility reflecting the ongoing tug-of-war between growth and inflation.

We’ll be back next week with a full analysis of the FOMC meeting. In the meantime, here’s hoping for an end to the shutdown.

Macro Job Board

This position will serve on the Global Macro Team. Collaborating closely with Mr. Dalio on key initiatives, this small team conducts cutting edge macroeconomic and markets research. The research directly impacts the DFO’s investments, and much of it is published externally and read by the top policymakers and thinkers globally.

In this role, you will serve as the sole G10 FX strategist based in our NYC office, working in close collaboration with your counterparts in the UK. You will monitor and review global macroeconomic developments, central bank policies, and geopolitical events, and translating these insights into actionable FX strategies.

You will be partnered with our senior analysts and traders to assist in identifying investment opportunities in the equity, index, and options markets. You will learn to perform in-depth company analysis around future catalyst events and provide real-time opinions on breaking news throughout the trading day.